This article explains how to calculate the factoring fees of a factoring proposal. It covers the three most common proposal fee types: flat-rate, variable-rate, and discount-plus-margin. We cover the following:

- How does factoring work?

- Typical rates and advances

- How to calculate factoring fees

- Additional fees

- Rates vs “Cost per dollar”

1. How does factoring work?

This article assumes that you are already familiar with factoring and know how it works. Here is a short summary in case you need a refresher.

Factoring companies finance your invoices by purchasing them in two installments. The first installment is called the advance and covers 70% to 90% (varies) of the invoice. It is deposited to your bank account soon after you submit the invoice to the factor.

The remaining 10% to 30% that was not initially advanced is deposited to your account, less a finance fee, once the invoice is paid in full.

2. Typical rates and advances

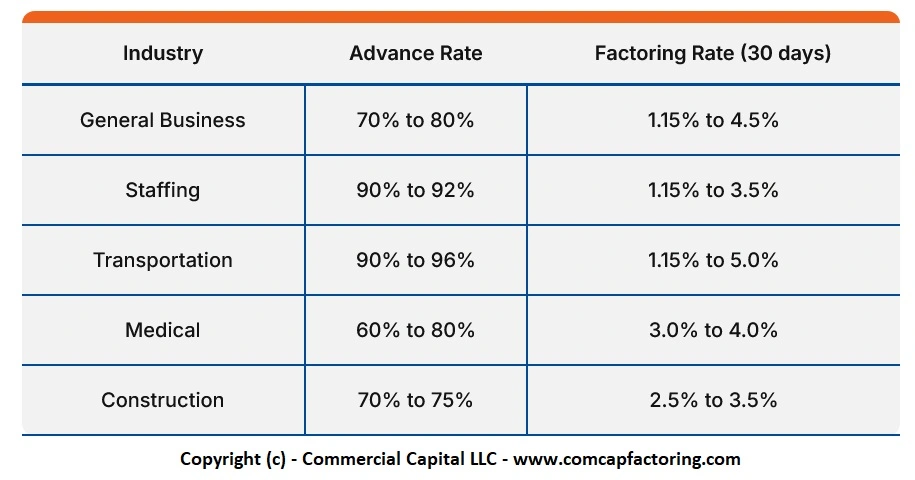

Factoring companies always present their finance rates accompanied by an advance rate. The following table gives you an idea of common rates and advances for different industries.

Note: Table can be scrolled left/right on mobile devices. Tap on screen if scrollbar does not appear. Click here for an image of the table.

{kind=link}

3. How to calculate factoring fees

Most factoring companies use one of three common pricing structures in their proposals. The structures are called fixed-rate pricing, variable-rate pricing, and discount-plus-margin pricing. In this section we describe how each pricing structure works and how to calculate the fees for each structure.

a) Flat-rate / Fixed-rate

The flat-rate structure is the simplest to understand. The factor quotes the client a flat rate for the service. Your company pays the flat-rate fee regardless of when the customer pays the invoice. Consequently, your costs per invoice are fixed. It costs the same finance rate to finance an invoice for 5 days as it does to finance it for 90 days.

Factors commonly offer this fixed-rate pricing to transportation companies. However, it is also available to companies in other industries, as long as customers pay predictably.

The cost is calculated by multiplying the invoice value by the fixed-rate price. Let’s assume that a factor charges a client a 4% flat rate. A company that factors a $1,000 invoice would pay $40 in fees to finance that invoice. The calculation is as follows:

- $1,000 x 0.04 (4%) = $40

b) Variable-rate / time-based

The variable-rate structure is the most common type of pricing in the industry. With variable, time-based rates, the financing rate for an invoice increases with the length of time the customer takes to pay the invoice. Consequently, an invoice that pays quickly costs less to finance than an invoice that pays slowly.

Time-based proposals can be presented in several ways. Some examples include:

- 1% per 10 days

- 2% per 20 days, 0.1% per day thereafter

- 2.5% per 30 days, 1.25% per 15 days thereafter

Understanding these proposals is straightforward. The first example charges 1% for each ten-day block that the invoice is unpaid. If the invoice pays in 1 to 10 days, the rate is 1%. If it pays in days 11 to 20, the rate is 2%, and so on.

The second example charges 2% if the invoice pays in 1 to 20 days, but adds 0.1% for each day after day 20. So an invoice that pays in 25 days has a rate of 2.5%, and an invoice that pays in 30 days has a rate of 3%.

The last example charges 2.5% for an invoice that pays in 1 to 30 days. The charge increases to 3.75% if it pays in 31 to 45 days, and so on.

To calculate the cost, follow these steps:

- Determine how long the invoice takes to pay.

- Calculate the factoring rate for a payment during that period.

- Multiply the invoice value by the rate for that payment period.

Here is an example. Assume that a company has a factoring rate of 1% per 10 days. They have factored a $1,000 invoice that is expected to pay in 30 days.

At 1% per 10 days, the rate for 30 days is 3%. Consequently, the cost is $30. The calculation is as follows:

- $1,000 x 0.03 (3%) = $30

c) Discount-plus-margin

Larger accounts receivable factoring lines are often priced using a discount-plus-margin model. This pricing model has two components: the discount and the margin.

The discount is a rate that is applied to the invoice gross value. The margin is a separate rate that is applied only to the advance. Margins are prorated on a daily basis but are quoted as a yearly rate. They are based on the prime rate and are quoted as a “prime + x%”, where x% is an increment determined by the factor.

Like variable rates, margin rates increase with time. Discount fees may be flat or variable. Examples include:

- 2% discount, prime + 2% margin

- 1.5% monthly discount, prime + 1.7% margin

- 1% per 30 days discount, prime + 1% margin

The cost of a discount-plus-margin plan is calculated by adding the cost of the discount to the cost of the margin. Note that it takes a few steps to calculate the cost of the margin.

Consider this example. A company has a discount-plus-margin rate of 2% discount with a prime + 2% margin. The advance is quoted at 85%. Assume that the prime rate is 4% and that you have a $1,000 invoice that pays in 30 days.

The cost of the discount is simple. It’s 2% of $1,000, which equals $20 (0.02 x $1,000 = $20).

Margin costs are prorated daily. To calculate the cost of the margin, we first calculate the daily rate. To do this, divide the yearly margin cost by 360 days (the length of the commercial year).

Now, multiply the daily rate by the number of days the invoice is open. This gives you the margin rate for the invoice. Lastly, multiply the margin rate for the invoice by the advance.

The steps are as follows:

- Yearly rate is 6% (4% + 2%)

- Daily rate is 0.0167% (6% / 360)

- Margin rate for invoice is 0.5% (0.0167% x 30 days)

- Advance is $850 ($1,000 x 85%)

- Margin cost for invoice is $4.25 ($850 x 0.5%)

As seen in step #5, the fees for the margin are $4.25. We add the $20 discount we originally calculated to get a financing fee of $24.25.

4. Additional fees

Some factoring companies offer simple fee structures. In these cases, your company pays the cost of financing and the costs of funds transfers only. Other factoring companies opt to charge a number of additional fees. Take these fees into consideration when calculating the total fees for your service or comparing factoring companies. Additional fees include:

- Due diligence

- Account maintenance

- Lockbox setup and maintenance

- Minimum invoice size

- Minimum factored volume

- Credit checks

5. The difference between rates and cost per dollar

One of the difficulties of comparing factoring proposals is that it is hard to do an equivalent (“apples-to-apples”) comparison. Comparing rates helps only if the proposals have the exact same advances and rating schedules and differ only in the finance rate. For example, compare:

Obviously the proposal with the 1% rate will cost less. But what about this situation:

Is the 3% “cheaper” than the 3.43% proposal? The fees are lower, aren’t they? However, the advances are also different. So, which one is better?

The reality is that they have the same “cost per dollar.” The cost per advanced dollar is the same, which makes the proposals equivalent. Consequently, you can select the advance rate that works best for your company.

Cost per dollar is the best way to understand the actual cost of factoring and to compare proposals. Learn more about how to determine the factoring cost per dollar.

Looking for Invoice Factoring?

We are a leading factoring company and can provide you with a competitive proposal. Get an instant online quote or call us toll-free at (877) 300 3258 to speak to a representative.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.