Summary: Factoring companies provide working capital to businesses by financing their invoices. They typically finance invoices by purchasing them in exchange for an immediate payment. Most factoring companies offer additional services, and some specialize in specific industries.

Key points about factoring companies:

This article explains how factoring companies work, their products, costs, and how to evaluate providers. We cover the following:

- What is a factoring company?

- What products do factoring companies offer?

- How does factoring work?

- How much does factoring cost?

- Types of factoring (recourse vs. non-recourse)

- Industries that use factoring

- Advantages of working with a factor

- Is factoring right for your business?

- How to evaluate factoring companies

1. What is a factoring company?

A factoring company specializes in financing accounts receivable. They typically work with small and midsize companies that have cash flow problems due to slow-paying invoices.

Most factoring companies offer financing to businesses across several industries. However, some providers specialize in specific industries, such as transportation and staffing. These providers offer customized plans that cater to the unique requirements of these industries.

Factoring companies are different from conventional lenders and use simpler underwriting criteria. Consequently, they are well suited to work with companies that would not qualify for conventional business financing.

2. What products do factoring companies offer?

Smaller and midsize factoring companies typically offer invoice factoring as their only product. However, some larger factoring companies also offer additional products, such as ledgered lines of credit, supply chain financing, and asset-based loans.

a) Invoice factoring

Invoice factoring is the main product offered by factoring companies. The solution is available to companies of all sizes with cash flow problems due to slow-paying business clients.

This solution provides financing using the client’s invoices as collateral. Consequently, the line has simpler qualification requirements and can be deployed quickly. We explain how factoring works in the next section.

b) Ledgered lines of credit

Ledgered lines of credit (LLOC), also known as sales ledger financing, help larger companies with cash flow problems. They offer more flexibility than factoring and operate as a revolving line secured by accounts receivable.

This solution is available to companies that invoice at least $300,000/month, are profitable, and have dependable financial controls. Note that this product is offered only by some factoring companies. Read “What is a Ledgered Line of Credit? How Does it Work?” to learn more.

c) Supply chain financing

Some specialized factoring companies also offer supply chain financing to their clients. The most common products are purchase order financing and supplier financing. These solutions help finance the cost of inventory and raw materials, enabling companies to pursue growth opportunities.

d) Asset-based loans

Larger factoring companies can also provide asset-based loans (ABLs). ABLs are typically available to lower-market and middle-market companies with at least $12,000,000 in yearly revenues. The facilities provide a comprehensive package that allows the company to finance accounts receivables, inventory, and machinery. Read “Navigating Asset-Based Loans: A Small Business Guide” to learn more.

3. How does factoring work?

Factoring companies usually finance your accounts receivable by purchasing your invoices. Consequently, transactions are often implemented as purchases rather than loans. This approach has several advantages and allows for quick turnarounds.

a) Two-installment transactions

The most common way of financing accounts receivable uses two installments. The first installment is called the advance and is funded when the factor buys the invoices. The advance covers 80% to 90% of the invoice and varies based on the transaction’s risk profile. The remaining 10% to 20% of the invoice, less a small factoring fee, is advanced as a second installment once the end client pays the invoice in full. This payment settles the transaction.

b) Single-installment transactions

Transactions in the trucking and staffing industries may be eligible for a single-installment structure. In these transactions, invoices are purchased with a single payment. This advance can be as high as 98% of the invoice. To be eligible for single-installment funding, your company must meet the factor’s industry and risk criteria.

To learn more, read “How Does Factoring Work?“

4. How much does factoring cost?

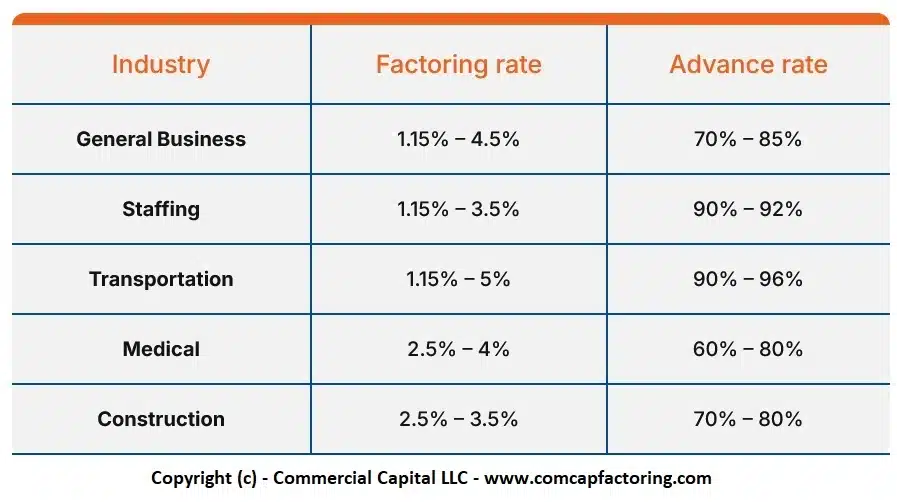

The cost of factoring is determined by your industry, financing volume, and the credit quality of your invoices. In general, fees range from 1.15% to 3.5% per month. These vary by factored volume and industry as the following table shows.

| Industry | Factoring rate | Advance rate |

| General Business | 1.15% – 4.5% | 70% – 85% |

| Staffing | 1.15% – 3.5% | 90% – 92% |

| Transportation | 1.15% – 5% | 90% – 96% |

| Medical | 2.5% – 4% | 60% – 80% |

| Construction | 2.5% – 4.5% | 70% – 80% |

Note: Click here for an image of this table.

{kind=link}

Factoring companies can structure their fees to suit your needs. For example, some transactions call for a flat-fee structure, while others benefit from a pro-rated model. Sample fees include:

5. Types of factoring (recourse vs. non-recourse)

One confusing feature of the factoring industry is that some companies finance invoices with recourse while others use a non-recourse transaction structure. Unfortunately, this subject is often misunderstood by prospective clients.

a) Recourse

In a recourse factoring plan, your company is responsible if your client does not pay for any reason. After 90 days, the factoring company can present an unpaid invoice to you for reimbursement.

b) Non-recourse

In a non-recourse plan, your company doesn’t have to repay the factor if the client does not pay due to a declared bankruptcy. This arrangement has some limitations, so read the factoring agreement carefully and consider getting legal advice. Note that a non-recourse plan offers no protection if the invoice is subject to a dispute or is simply late.

c) Which option is better?

The better option is ultimately a matter of opinion and preference. While non-recourse offers some protection against client bankruptcies, it comes at a price. Note that factoring companies avoid risky invoices altogether. It’s unlikely they would buy an invoice from a company that is at risk of bankruptcy. Consequently, the chances of using the non-recourse option are low.

6. Industries that use factoring

Factoring can be used in any industry where goods or services are sold to commercial clients and are paid for in net-30- to net-60-day terms. The following businesses and industries regularly use factoring.

7. Advantages of working with a factoring company

Working with a factoring company has several advantages, especially for small and growing companies. Factoring can provide financial stability and a platform for growth.

a) Improved cash flow

The core benefit of a factoring program is improved cash flow. The factoring advances provide your company with the funds it needs to run operations and grow.

b) Easy line increases

Factoring lines are adaptive and can grow to match your sales to high-quality customers. Furthermore, most line increases can be approved and deployed quickly.

c) Simple approval process

Factoring companies have a simplified underwriting process. This benefits small and midsize companies that don’t have substantial assets or a long track record. The most important requirements are a well-organized company and high-quality invoices.

d) Fast turnaround

Most new factoring lines can be established and funded in less than five days. Once the line is established, invoices for approved customers can typically be funded on the same day.

e) Additional services

Factoring companies can also provide additional services, such as helping clients manage credit risk effectively. In some industries, such as transportation and staffing, factoring companies can provide a full suite of solutions designed to streamline operations.

8. Is a factoring company right for your business?

Invoice factoring is not a general financing tool. It is designed to help companies with a specific set of circumstances. This solution may be right for your company if the following apply to your business.

a) High-quality invoices

Factoring companies can only finance high-quality invoices for delivered products and/or services. Note that pre-billed invoices or invoices for undelivered products/services cannot be factored. Invoices must be payable in less than 90 days, though less than 60 days is preferred. Lastly, the payment must be from a creditworthy commercial client or a government agency.

b) Cash flow problems

A factoring company can help you only if your cash flow problems are related to slow-paying invoices. Unfortunately, factoring won’t be much help if your problems are due to other reasons.

c) Have no other financing

Most conventional loans and lines of credit file a blanket lien that covers all assets, which includes accounts receivable. However, factoring companies must have a first-position lien on the invoices they finance. This situation creates a potential conflict of interest.

A factoring company won’t be able to finance your invoices unless your current lender is willing to agree to an inter-creditor agreement that subordinates their position on A/R. In our experience, most lenders won’t agree to this.

d) Have no serious tax problems

A factoring company can work with a business that has tax problems, provided the problems are not serious. The business must have a turnaround plan and may need a payment agreement with tax authorities.

e) Have no serious legal problems

Factoring companies can work with companies with legal problems, provided these problems are not serious. Furthermore, the legal issues must not threaten the company’s viability.

9. How to evaluate a factoring company

Working with the right factoring company is important to the success of your business. Consequently, you should evaluate potential partners carefully. Consider the following six questions as you interview factoring providers:

a. Do they work in your industry?

Most factoring companies describe themselves as generalists. However, most have industry preferences. When possible, work with factoring companies that have clients in your industry. This strategy ensures they know your client base, general credit, and payment habits.

b. Are their advances and factoring rates competitive?

The factoring industry is very competitive. Consequently, the advance and rate differences between proposals should be minor. You can quickly determine this through simple due diligence and by evaluating a few providers.

Be cautious of proposals that seem “very cheap” as they may have hidden costs. Ask the provider to outline all costs in their initial proposal.

c. Do they have minimums?

Most factoring companies can give you better pricing if you agree to finance a minimum invoice volume. However, the usefulness of minimums depends on your situation.

Minimums can work well for companies with predictable revenues. However, they can be expensive for companies with unpredictable sales. It’s best to agree only to minimums you are sure your company can cover.

d. How quickly can they set up your account?

Most factoring companies can set up an account in three to five days. The main issues affecting the length of the setup process are:

- How long it takes you to review documents and provide information

- How long it takes your clients to acknowledge the Notice of Assignment (NOA)

e. Can they provide references?

It is a good practice to ask your prospective factoring partner to provide you with client references in your industry. These references can help you determine if the factoring company is a good fit for your company.

f. How long have they been in business?

Lastly, look at how long your factoring company has been in business. It is best to work with a company that has been in business for a decade or longer. This longevity shows they have experience managing a portfolio in different economic environments.

Are you looking for a factoring company?

We are a leading factoring provider and can offer low rates and high advances. For more information, get an online quote or call us toll-free at (877) 300 3258.

Marco Terry is the Managing Director of Commercial Capital LLC and has over two decades of experience in asset-based finance. He has worked with small and mid-sized companies across the United States, Canada, and Australia. Marco holds a Master of Science in Finance.